Breaking Down DeFi: Stablecoins

Breaking Down DeFi: Stablecoins

What they are and stablecoin models

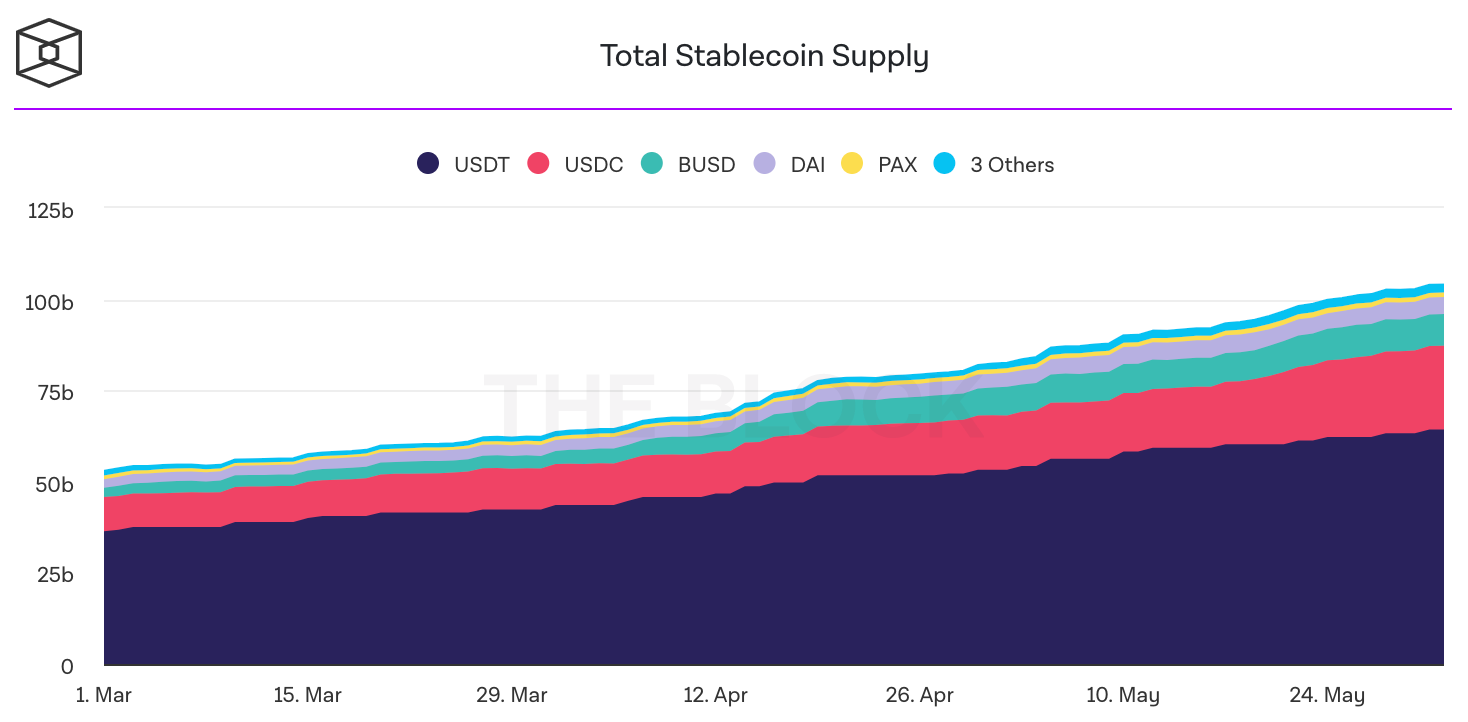

The total supply of stablecoins surpassed $100 billion, marking an increase from $30 billion since the beginning of the year. An essential part of the crypto ecosystem and one of the most interesting areas, stablecoins represent a significant change away from the ‘traditional’ forms of money we are so accustomed to. While at the same time, however, remaining familiar.

Source: The Block

Stablecoin 101

To be considered a form of sound money, an asset must meet three attributes; 1) store of value, 2) unit of account and 3) medium of exchange. What has traditionally held back cryptocurrencies from meeting all three is volatility. While it may be used as a unit of account and medium of exchange, volatility especially hampers them to be considered a healthy store of value (as proven with the most recent drawdown).

Enter stablecoins. A stablecoin is a crypto-asset with a stable value designed to mimic the price of a fiat currency. It is said to be ‘stable’ given that it is pegged against something, in most cases a fiat currency. They are essentially a digital representation of fiat currency that lives on blockchains. They share all of the same features of a cryptocurrency but without volatility. Hence making it a far more appealing store of value and ultimately a good form of money.

So far, stablecoins have seen adoption, especially with traders, due to a number of use cases:

By exchanging an asset for a stablecoin, traders can protect their profits and capital from volatility.

Not all exchanges have fiat on-ramps. Stablecoins provide a solution around such.

Meanwhile, in DeFi, stablecoins offer a means of collateral against loans while others may lend and earn yield.

Stablecoin Models

There are three models of stablecoins.

Off-Chain

Off-chain stablecoins are issued by a centralized third party and backed by a fiat currency, commodity or some other asset that the issuer holds in reserve. The reserve could be made up of a single asset or a basket of multiple assets. Typically, however, these are pegged 1:1 to a single fiat currency. So for every unit held in reserve, an equal amount of the stablecoin is issued. An example is USDT. Pegged 1:1 to the US Dollar, USDT has seen the most traction due to it being the first stablecoin issued. Most recently, USDT surpassed a market cap of $50 billion.

Off-chain stablecoins have seen the most adoption and are the most stable when compared to the other models discussed below. However, they are centralized, a characteristic many are not comfortable with. One must trust the issuing third party that the reserves they claim to have are accurate. With USDT for example, question marks remain over how much USD is actually held in reserve. And while USDT releases transparency reports, some still remain sceptical.

On-Chain

On-chain stablecoins are backed by trustless, decentralized crypto-assets yet still pegged against a fiat currency, the US dollar in most cases. For this to work, users deposit collateral into a smart contract and a number of stablecoins are issued in return. Unlike off-chain stablecoins, a user has to deposit more than 100% of the supported crypto-assets in a smart contract as collateral (over-collateralization).

Take Makers DAI as an example. A decentralized, crypto-collateralized stablecoin, DAI’s value is pegged to $1. If a user wishes to get $100 worth of DAI, they must deposit $150 worth of ETH.

The drawback with on-chain stablecoins is that the assets used as collateral, such as ETH, are prone to volatility. Hence why the user must provide excess collateral. By having excess collateral, one can guard against a sudden price drop of the collateral assets. And in such cases, the users collateral will be sold in order to maintain the stablecoins value. While over-collateralization is seen as a drawback, it is this mechanism that facilitates not having to trust a third party.

Algorithmic Stablecoins

The most experimental and innovative of the three categories, algorithmic stablecoins use algorithms to maintain the peg. They are oftentimes not backed by anything “other than the expectation that they will retain a certain value” or backed partially by their own native token. The supply is usually flexible. As the price of the stable asset moves above $1, the algorithm contracts the supply reducing the price back to the target level ($1). The opposite occurs when the price moves below $1 (the supply expands). Algorithmic stablecoins may also be governed by incentives that incentivize market participants to buy or sell the asset in order to maintain price stability.

One example is Ampleforth. Known as rebasing, Ampleforth automatically adjusts the circulating supply in response to demand. However, this does not dilute the value of the individuals holding as everyone’s wallet holding AMPL is affected. Your percentage ownership of the network, therefore, remains fixed.

Many other algorithmic stablecoin models have been implemented since such as Empty Set Dollar and Fei to name a few. However, while they are decentralized, this category of stablecoins is still very experimental with many failing to maintain the peg.

This is a very, very high-level overview of algorithmic stablecoins. There are a number of methods that algorithmic stablecoins utilize to maintain their peg. These deserve an entire blog post in their own right.

Looking forward

To conclude, the area of stablecoins will no doubt continue to evolve over the coming years. We could see a mix of the above categories whereby there is both reserve and algorithmic mechanisms employed to maintain the peg. The percentage amount of collateral that needs to be fronted could change away from the traditional 150% as seen with Makers DAI. Not to mention, their importance will only increase. They are driving adoption in the crypto space, creating more stable systems and providing a means to access stable assets in regions where fiat currencies are prone to volatility such as Venezuela.

Stablecoin utilization is also expanding beyond the realm of crypto. We will increasingly see stablecoins be used for the likes of remittances, lending and micropayments given the lower fees and faster transaction times. What remains now, beyond continued experimentation and innovation, is improving accessibility.